🏡 Here's how the Fed lost the war against housing inflation

You know the backstory

Fed tried to increase rates to crash housing.

You might remember Jerome Powell saying this:

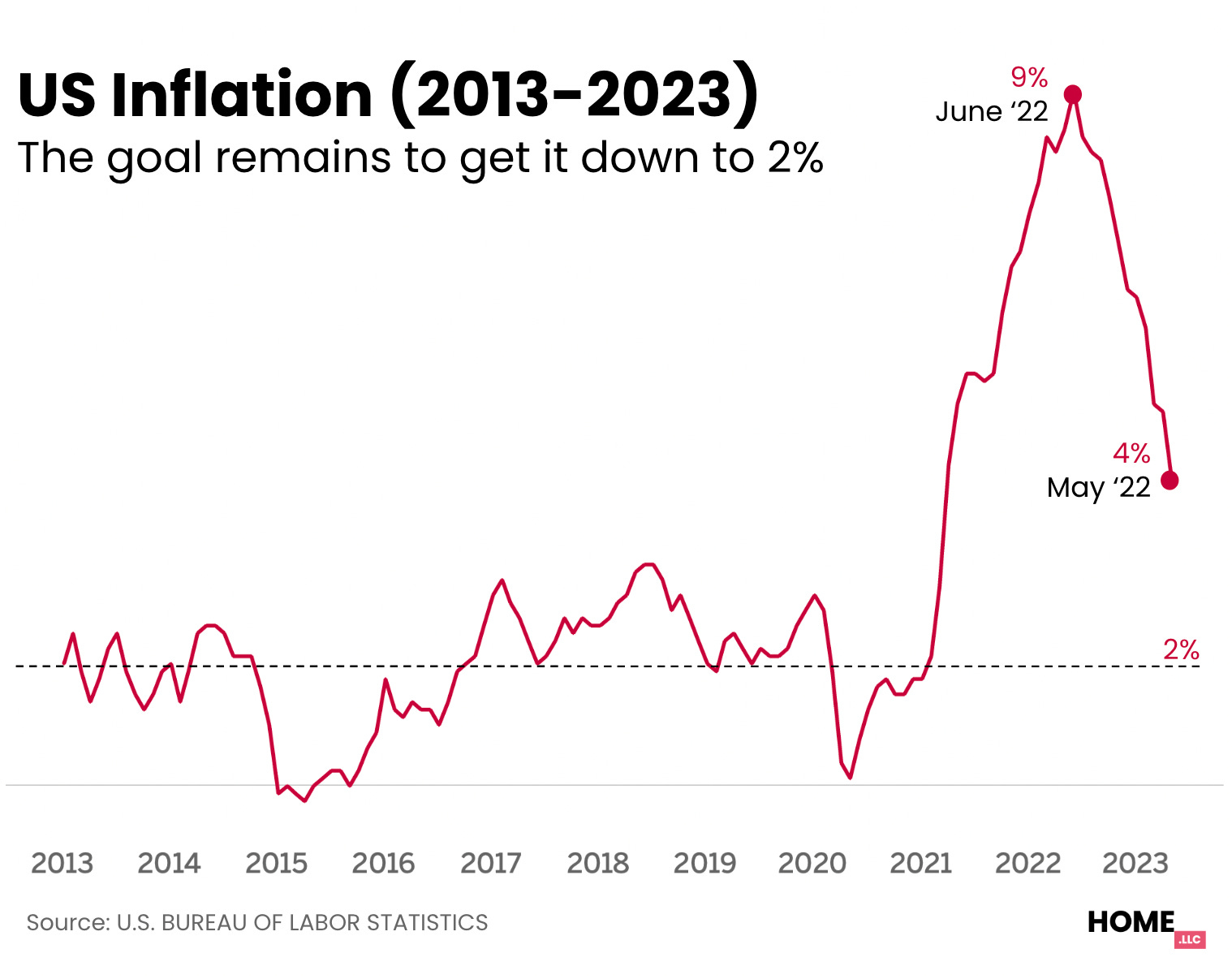

Shortly before this in 2022, inflation had peaked at 9% and he wanted to bring it to 2%.

Seems like Powell’s thesis was that crashing the housing market should reduce inflation because housing is the biggest component of inflation.

But, the housing market didn’t crash

Due to the Fed’s efforts, home prices corrected by just 5%

We could see this from a mile away. We predicted that home prices would STILL increase by 4% in 2023 even when they were correcting in Sep. ‘22.

Why? Because high-school economics. Prices increase when demand is higher than supply.

Increasing rates from 3% to 7% reduced demand. In fact, home purchases in 2023 will be significantly lower than the previous years.

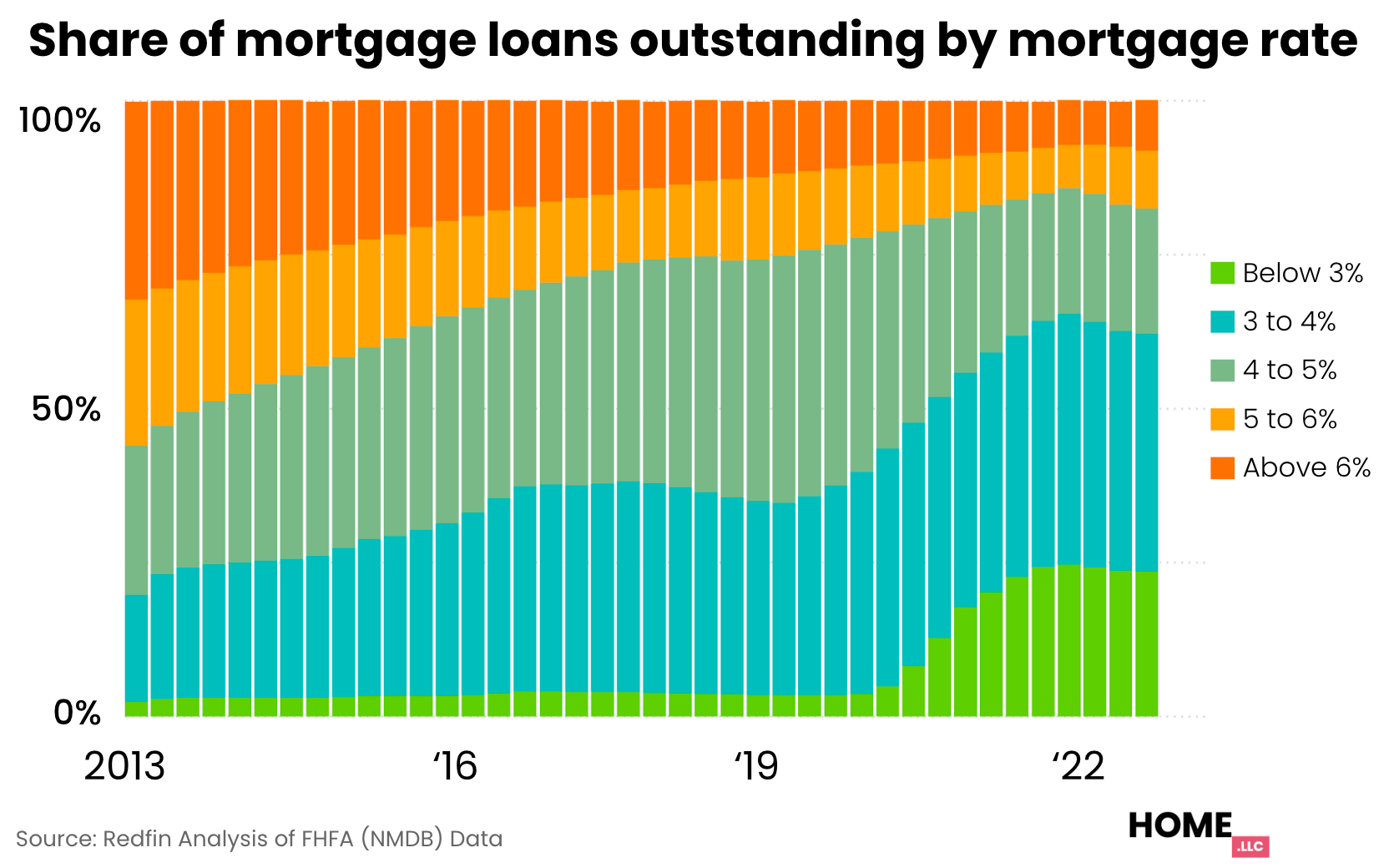

But, increasing rates reduced supply a LOT more. Almost all of the country is locked at sub-6% rates, why would they sell?

So, Powell is pausing. But not really.

The Fed is clearly caught between a rock and a hard place. If they keep increasing rates, they will crash small banks & commercial real estate, which won’t directly reduce inflation. If they drop rates, inflation will skyrocket again.

So, the Fed did the only thing they could. Pause, without calling it a pause.

Meanwhile, home prices are already increasing in 82% counties across the US.

And, the housing’s component of inflation won’t start reducing for a while, just because of the flawed way the BLS counts inflation, which we explained previously.