🏡 Will SVB's crash help or hurt the housing market?

In Summary

SVB’s crash and bailout will slow the home price crash, but the Fed will decide.

Short Term: Home prices will find support due to a sudden decline in rates

Mid-Term: Home prices will keep declining till Fed keeps hiking rates

Long Term: Home prices will skyrocket once rates start declining

Short Term: Home Prices Find Support

The SVB collapse has eroded the people’s faith in banks. As a result, treasuries prices have jumped, and yields have fallen as investors flock to safer assets like the treasuries.

The mortgage rates are tailing the decline of the treasuries yield. Housing Affordability is improving as mortgage rates decline, supporting home prices.

Mid Term: Home Prices Keep Declining

However, Home Prices will keep declining further.

As inflation rose 0.4% Month-on-Month in February, Fed will keep increasing rates, albeit slowly.

Housing contributes to 45% of inflation, a share that has grown for months. So Fed is keen on demand destruction to cool the housing market down.

To add to Fed’s concerns, the Job market remains robust.

The unemployment rate remains low.

Wage growth is high at 6.1% YoY.

The Labor Demand-Supply gap has risen to 5 Million.

Fed’s tightening will continue until the job market is tamed.

Long Term: Home Prices Will Skyrocket

In the long term, home prices will keep rising.

Inflation will be tamed

Inflation will hit Fed’s 2% target sooner rather than later. Fed will follow that up with a pause on rate hikes.

Housing data is severely lagged, and, as expressed by Powell in February, we will see housing inflation decaying soon.

Under assault from the Fed, the Job market will be tamed in the long term. We may already be seeing the first cracks. A black-swan event may accelerate the process.

Further, the 2024 presidential elections are inching closer every day. As a result, the administration is highly motivated to control inflation in the lead-up.

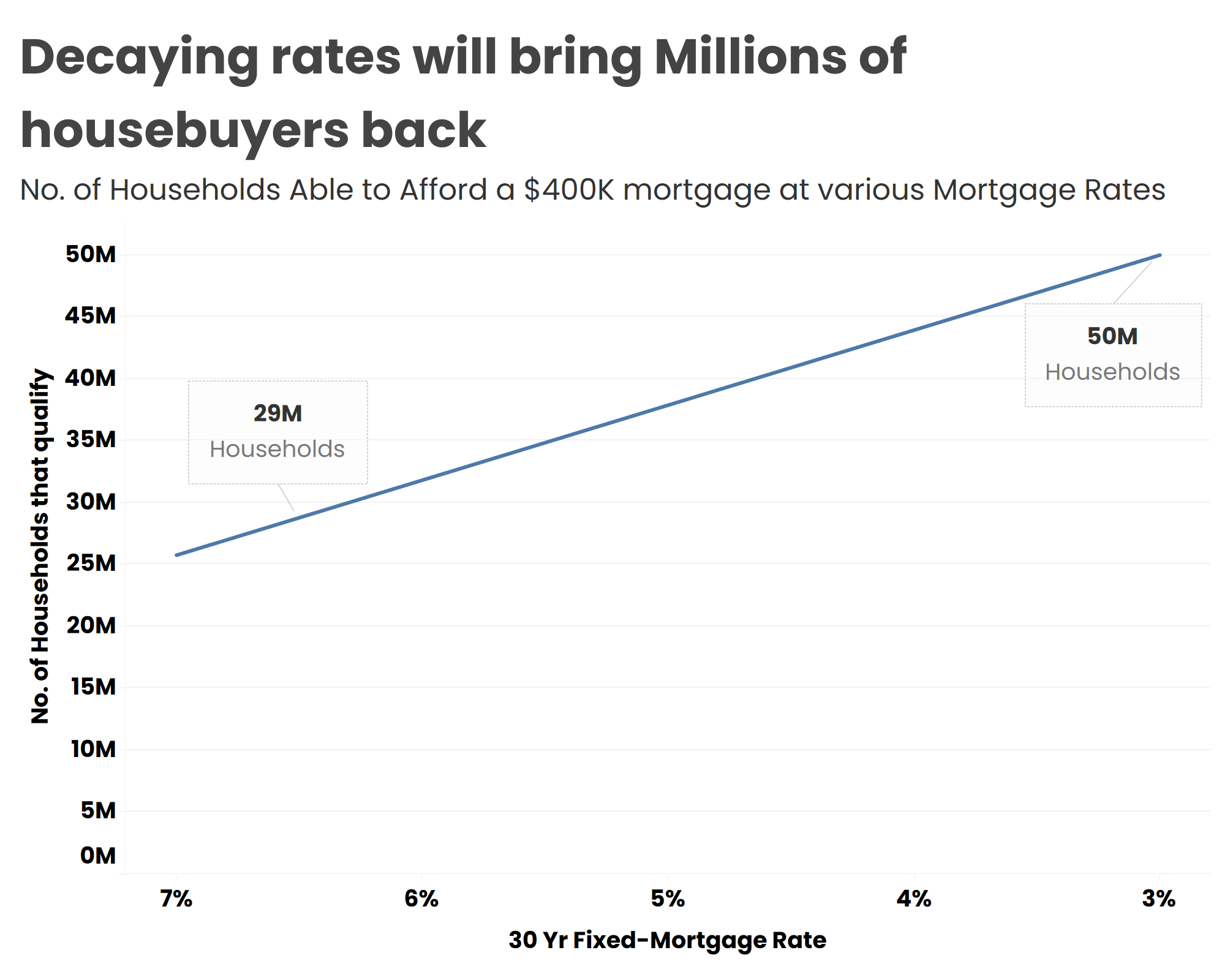

Demand will return. Supply may fall short.

When rate hikes cease, demand will rapidly increase.

Once rates drop below 5%, 10 million homebuyers can return to the market. At 3%, 20 Million households can return.

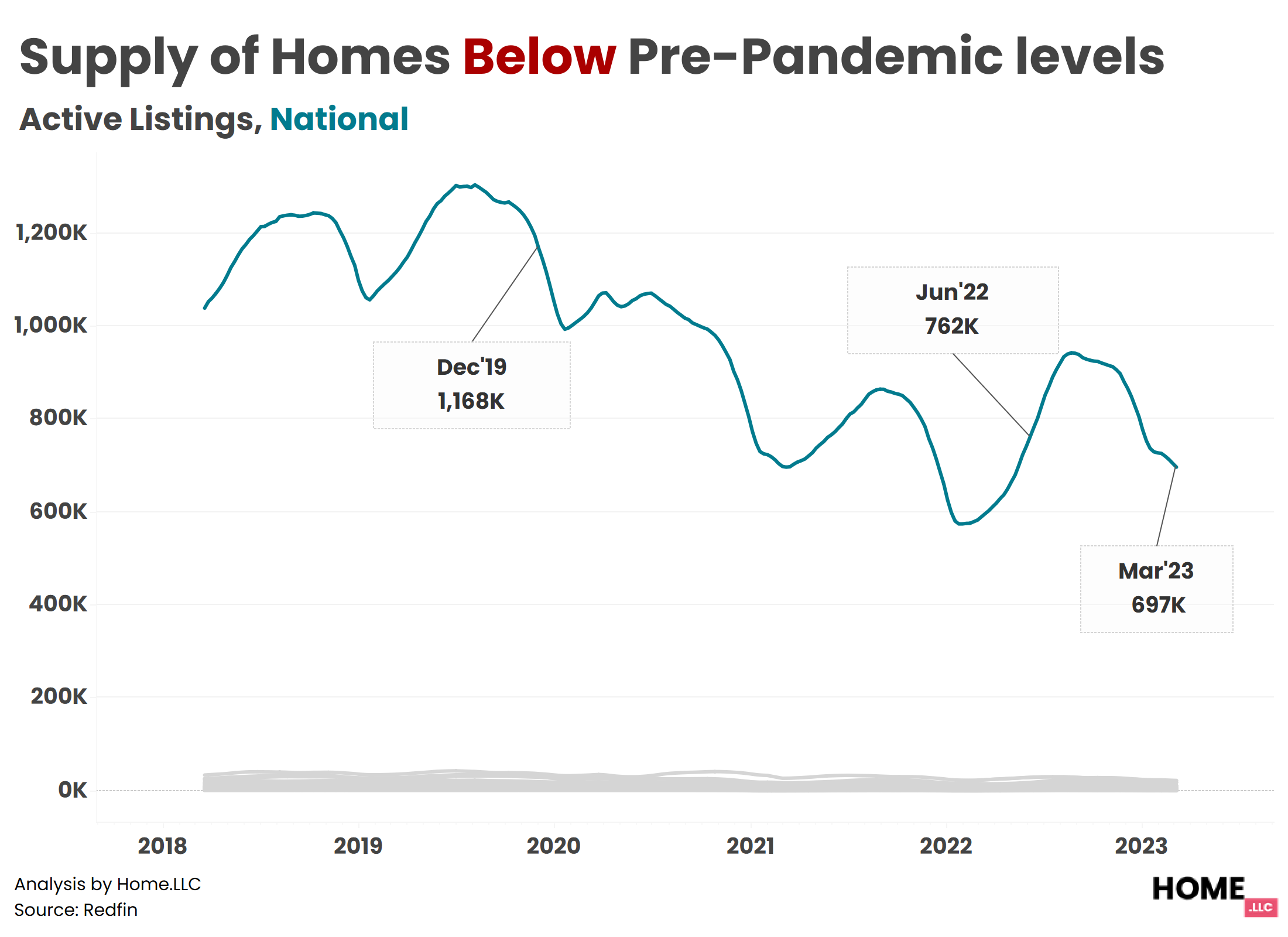

Nevertheless, the housing supply is still near an all-time low. There are 40% fewer homes for sale compared to their pre-pandemic level.

We’re bearish in the short term but bullish in the long term. How about you?

Note: All statements above are subject to revisions based on changing assumptions and market conditions. Figures could be rounded by +-10% to improve readability. We are neither a tax nor a financial advisor, and none of our statements should be interpreted as tax or financial advice.

90098699556lso, I will pledge next week, your market insight is spot on, and I would like to repost it to about 30K or so RE agents across America. Hopefully they will enjoy it and pledge as well. Would you have any problems with me doing that. Additionally, I am getting a startup I invested in some capital next week in NY. We will host professional dashboards and homeowner dashboards, and I would like for your data to be syndicated out to them with your permission and fees.

NIK, we have only spoken once on the phone, but I have read your material and I know that you have tremendous, but I have some questions on your recent call on the future direction of housing prices.

First, what makes you think that all the other regionals are not insolvent if they were forced to take proper marks on their tier one assets. At least 500 banks would be shuttered on Monday afternoon if the current administration let Regulators have access. This is not like the last criminal circus that banks caused, but had the FED not stepped in to start buying the Treasuries off lenders balance sheets at a premium, the S&P would be 9% lower.

Also, when we round out at approximately a 28% decline in housing from peak to trough, is that the support level you are utilizing to gauge this huge burst you expect in long term prices. After building support at much lower levels, why would the housing market have this meteoric rise, versus... moving higher at the same growth rates as household income?

Either way, you are a super-sharp guy, and I would like to discuss an opportunity that may become available in the very near future.

Thanks Nik..

Jimmy D.