🏠Equity Shock⚡?

Does a stock market crash lead to a fall in home prices?

Home prices rise even during a stock market crash

We looked at 9 previous instances when stock markets crashed over a 12-month period. Home prices went up during 8 of them.

Turns out that home prices are impervious to movements in the equity markets!

Home.LLC gets featured in Fortune Magazine

Lance Lambert reports on how the housing market will be affected by the imminent end of 2 government support programs for homeowners - (a) the foreclosure moratorium, which prevents foreclosures of federally-backed mortgages, and (b) the mortgage forbearance program.

He asked Home.LLC how this would affect the housing market. Our response:

“High positive home equity among delinquent homeowners results in lower likelihood of foreclosure since people can refinance or sell the home to avoid defaulting on their mortgage,” says Nik Shah, CEO of Home.LLC. Those who do choose to sell are unlikely to shift the market. The forecasted uptick in inventory, he says, “isn’t much given that inventory is at a 40-year low. So, we project that home prices will continue to grow rapidly even if the forbearance program ends.”

Read the full piece here.

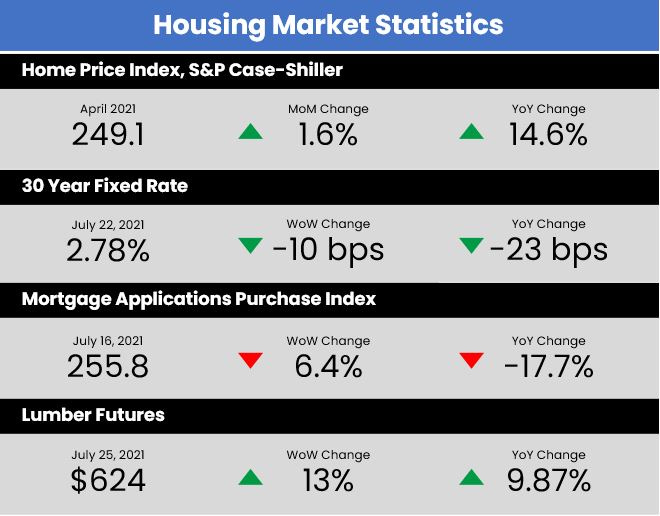

The housing market continues its hot streak

Home prices have grown 14.6% over the past year, according to the S&P Case-Shiller Home Price Index. Mortgage rates have declined by a staggering 10 bps just over the past week. Mortgage purchase applications are down a 6.4% over last week, and a whopping 17.5% on a year-on-year basis. After a sharp decline over the last month, lumber prices are up 13% this week, and 9.8% year-on-year.

Housing completions are at a record low

Single family housing inventory is slowly improving. But Rick Palacios of John Burns Real Estate Consulting notes that completed homes - i.e., homes that are ready to be put up for sale - account for only 11% of the total inventory.

Bottom line: Do not expect housing supply to ease up just yet.

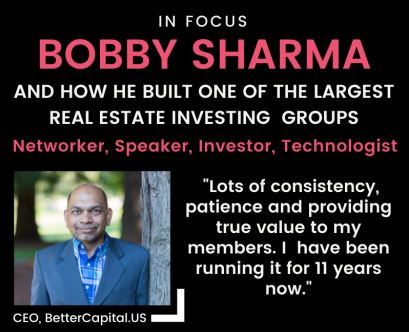

Home.LLC Exclusive Interview: Bobby Sharma

We talked to Bobby Sharma, CEO of BetterCapital.US. Here’s an excerpt from our wide-ranging chat:

Q. What asset classes in real estate are you going to allocate in? And in what asset classes are you planning to decrease your allocation in real estate?

A. I am mostly a buy-and-hold person. I will now focus on buying high-quality homes/assets that hold value for a long time.

You can find the full interview here.

2021 housing boom is very different from 2006 bubble

Home prices rose steeply in the early 2000s, only to crash during The Great Recession. With prices similarly high in 2021, are we in a similar moment? Molly Boesel of CoreLogic compares the 2006 and 2021 housing booms, and establishes a crucial difference - affordability.

“In 2006, a household spent 25% of their income on a mortgage payment, but in 2021, that ratio dropped to 17%.”

Higher affordability coupled with low housing inventory means that the home price gains in 2021 are sustainable, and that prices should continue their upward trajectory.